Dear Reader,

Last week, the U.S. Senate quietly passed the 21st Century ROAD to Housing Act – the largest housing package in decades.

Its goal is to improve housing affordability, and it passed with an overwhelming majority of 89–10.

Both sides voted for it. The Trump administration has issued a statement supporting it.

It still needs to go through the House of Representatives, but there’s a good chance this Act will soon become law.

Now, there are good parts of this Act, which I’ll get to in a bit.

But first, I need to talk about the “housing boogeyman” this Act supposedly addresses.

Maybe you already know what I’m talking about…

The institutional investors.

You know, Blackstone and the other private equity investors…

The greedy corporations that are supposedly buying up all the homes and driving up prices.

The Act restricts large institutional investors from buying new single-family homes, with the exception of doing so to increase rental supply (and even then they have to sell those homes within 7 years).

Look, I get it.

Home affordability is an emotionally charged topic. Shelter is a basic human need after all.

But these institutional investors are nothing but a convenient boogeyman used by those who either don’t understand the housing market – or are just looking to score political points.

“Today Democrats are introducing legislation to stop Wall Street from snapping up homes in bulk and jacking up rent for families”

- Senator Elizabeth Warren

“Hedge funds are driving up home prices and rents across America as they gobble up single-family homes. They are a significant factor in killing the dream of home ownership and must be stopped”

- Senator Jeff Merkley

So today, I’m going to show you why “institutions driving up home prices” is a myth…

And the real reason why housing has become increasingly unaffordable.

The Numbers Behind Institutional Investors “Buying Up All the Homes”

If you actually look at the numbers, the story falls apart fast.

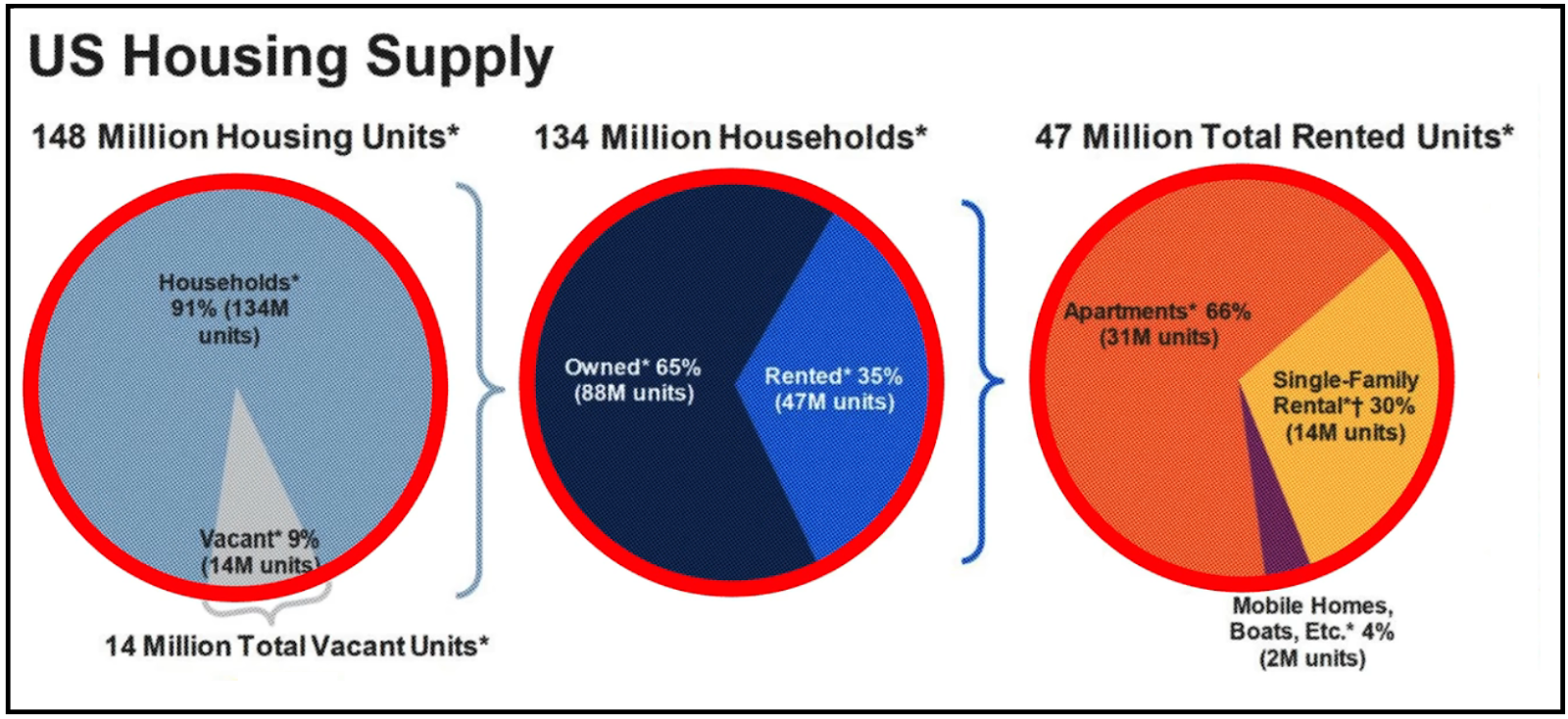

There are about 148 million housing units in the United States.

Out of those, about 47 million are renter-occupied.

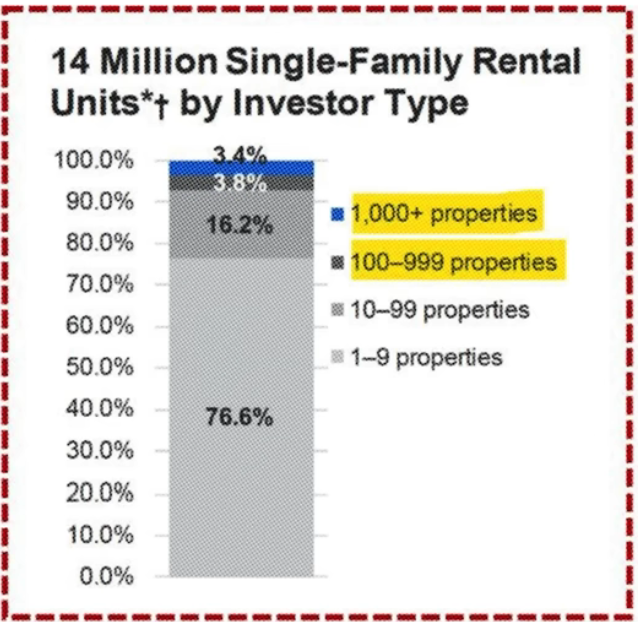

And out of those 47 million renter-occupied units, only about 14 million are single-family rental homes.

So right away, when it comes to single-family homes, we’re not talking about some giant slice of the housing market.

We’re talking about a relatively narrow subset.

And within that subset, the overwhelming majority is not owned by giant firms.

About 76.6% of those 14 million single-family rentals are owned by investors with just 1 to 9 properties.

Another 16.2% are owned by people with 10 to 99 properties.

That means nearly 93% of all single-family rental homes are owned by landlords with fewer than 100 properties.

These investors aren’t Blackstone or other giant private equity funds.

Lots of them are just regular mom-and-pop investors. I know plenty of people with 5 – 12 properties just from working hard and constantly saving and investing over the years.

The really large owners – those with 100 or more properties – account for just 7.2% of that 14 million slice.

And by the way, the Act defines large institutional investors as those owning at least 350 properties, so we’re probably looking at somewhere closer to 5% of the market.

Sure, that’s not nothing.

But it’s nowhere near some all-powerful Wall Street cartel cornering the housing market.

It’s just a relatively tiny piece of the market that has been blown up into a giant political scapegoat.

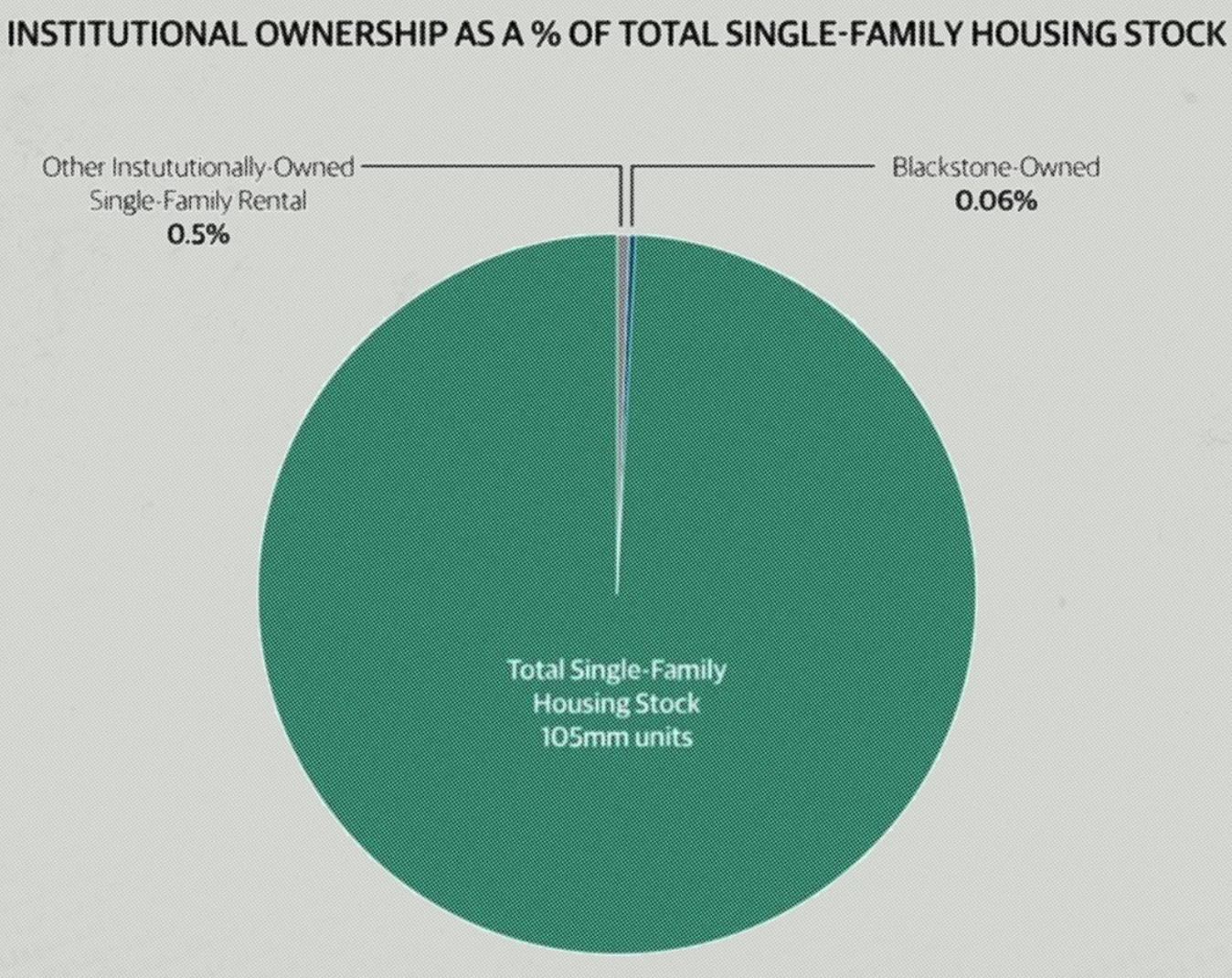

And the favorite villain of all – Blackstone – accounts for a negligible 0.06% of the entire single-family market.

Recent market data makes that even clearer.

In January, there were roughly 600,000 more home sellers than buyers nationwide – a 44% gap, one of the largest imbalances Redfin has recorded.

This is not a market that looks like giant firms are vacuuming up every available home.

If that were the real story, you wouldn’t expect to see a market where sellers so heavily outnumber buyers.

On top of that, there’s also a huge economic contradiction behind this narrative that most never even think of.

Why It’s Impossible for Institutional Investors to Drive Up Both Rent and House Prices

If an institution goes in and buys up all the vacant single-family homes and puts them up for rent…

That means more properties being available for rent – aka more rental supply – which pushes rental prices down.

But if there are fewer rentals available and they're just available for purchase, that makes rental prices go up, but it pushes single family purchase prices down.

So those two claims pull in opposite directions.

It’s economically incoherent to treat institutional buying as the obvious explanation for both rising home prices and rising rents.

You can argue that institutional buying affects access to ownership. Fine.

You can argue it changes the character of neighborhoods. Also fine.

But the idea that institutions are simply making housing unaffordable across the board is lazy, flawed thinking.

So, what are the real reasons behind the lack of housing affordability?

It once again comes down to anti-free-market forces. Two of them, in fact.

The Two Anti-Free-Market Forces Perpetuating the Problem

The first is artificial supply constraints – largely local regulations that have made it harder, slower, and more expensive to build housing.

And the good thing about the 21st Century ROAD to Housing Act is that it tries to address this issue by cutting regulatory friction – things like streamlining environmental review and modernizing rules for manufactured and modular housing.

But by restricting institutional investors, they may be actually decreasing supply and “locking up” the market even more – especially with the big buyer-seller gap we’re seeing right now.

And at the same time, the Act is also amplifying the other anti-free-market force driving up prices – artificial demand.

This happens through subsidized credit, special financing channels, low-down-payment structures, and all the various ways Washington tries to help people “afford” more house.

The intentions are good.

But the knock-on effects are causing the very problem they’re trying to solve.

And this Act makes it worse.

It expands government-backed financing and makes it easier for more buyers to access credit.

In other words, it makes it easier for more buyers to bring more borrowed money into a market where supply is still constrained.

This means more artificial demand – and higher housing prices.

So while the Act does have some positive things…

In the end, like many political efforts, it contradicts its own goals by going against economics.

Of course, no politician will ever vote against these artificial demand regulations.

Because even though it may drive down prices, many voters will “feel” poorer, and they’re not going to like that.

And so, the cycle continues.

Populism leads to economically irrational policies, which perpetuates the problem – which then leads to more populism.

You may not be able to change the incentives driving this system.

But you can at least understand them – and position yourself accordingly.

Until next time,

-Joe Brown

Heresy Financial

Letters From a Heretic

Don't miss out!

Get our free, no-spam, weekly digest. Unsubscribe anytime. Never miss out on crucial financial insights!

I really enjoyed this course. Joe has a special skill at teaching. He is very concise which I appreciated. The only thing I was an experienced investor at was real estate so I am a complete newbie to all the other assets he touches on in this course. I feel much more confident now about investing in the stock market, his explanation of options and hedging was really insightful as well.

I loved this course. It was knowledgable and gave me a new perspective on capital management. The portfolio you put together made so much sense to me, and it's kind of surprising that it's not more widespread. I really liked how you broke down mainstream portfolios and explained the pros and cons of each. It helped me get a better sense of the investment landscape and made me feel more confident